Eigenvalues and eigenvector of a positive-definite, real valued and symmetric matrix

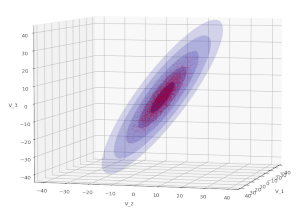

A bivariate normal distributions [BVD] is governed by a central positive symmetric matrix. This matrix is a covariance matrix which describes the variances and correlation of the BVD’s marginal distributions. The contour lines of the probabilty density function of a BVD are ellipses. The half axes and the orientation of these ellipses are controlled by the eigenvalues and eigenvectors of… Read More »Eigenvalues and eigenvector of a positive-definite, real valued and symmetric matrix